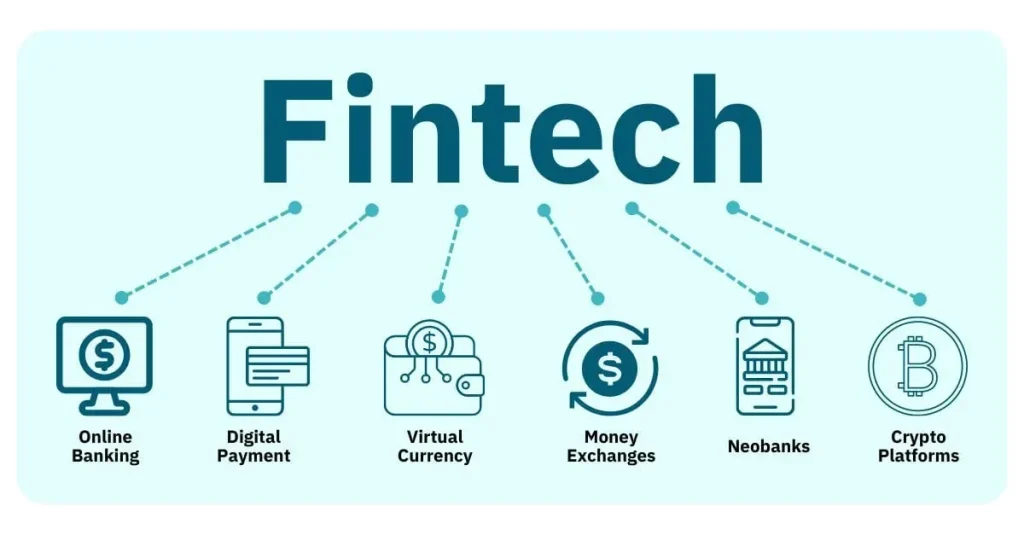

FinTech technologies are redefining how people and businesses access financial services, blending digital capabilities with trusted data to unlock faster, smarter outcomes. Digital banking innovations are reshaping everyday experiences, moving from branch-centered models to app-led, real-time interactions. Beyond faster payments, the landscape is driven by secure APIs, data networks, and scalable platforms that enable new services. As new capabilities scale, institutions must balance speed with governance to protect privacy and maintain trust. Understanding these shifts helps teams prepare for broader adoption, regulatory considerations, and sustained customer value.

In Latent Semantic Indexing terms, the topic is best described as a network of related concepts rather than a single label. This second paragraph introduces the subject using alternative phrases that map to the same idea: a financial technology ecosystem built on open data, modular architectures, and intelligent automation. AI-powered decisioning, blockchain-based settlements, and open banking data sharing are accelerating capabilities like automated lending, real-time risk assessment, and cross-border payments. The practical focus for organizations is governance, regulatory readiness, and user-centered design as they experiment, scale, and deliver trustworthy digital experiences.

FinTech Technologies in Action: AI in Finance and Digital Banking Innovations

FinTech technologies are redefining how people and businesses access financial services, weaving AI, machine learning, and secure mobile interfaces into everyday banking. By combining digital banking innovations with cloud platforms and open APIs, providers can deliver faster payments, real-time insights, and more accessible credit options. This convergence is a key driver of fintech disruption, transforming traditional banking into consumer-tech experiences.

From AI-powered credit scoring to biometric authentication and personalized financial advice, these technologies use data-driven decisioning to reduce friction and risk. Banks and fintechs adopting modular, API-first architectures can test new services—such as automated savings, cross-border payments, and wallet integrations—while maintaining strong data privacy and security.

To thrive, organizations should align with regulators and invest in governance, model transparency, and responsible AI practices that address bias and explainability as AI in finance becomes more pervasive.

Open Banking, Blockchain Payments, and Smarter Risk Management

Open banking acts as an ecosystem accelerator, enabling secure access to customer data through standardized APIs. This collaboration among banks, fintechs, and payments providers unlocks new revenue streams and creates tools that aggregate accounts, analyze spending, and optimize cash flow. For consumers, it translates into better pricing, more choice, and the benefits of financial data sharing that fuels digital banking innovations.

Blockchain payments illustrate near-instant settlement and improved transparency, challenging traditional correspondent banking. As cross-border transfers and smart contracts mature, interoperability with existing rails and regulatory alignment will shape mainstream adoption. RegTech and risk-management solutions help institutions govern data privacy, cybersecurity, and compliance across this evolving landscape.

AI in finance continues to augment decisioning with predictive analytics and personalized recommendations, complementing open banking data to tailor lending, insurance, and investment products while promoting fintech disruption in a responsible, governance-led manner.

Frequently Asked Questions

How are digital banking innovations and open banking reshaping the consumer banking experience?

Digital banking innovations deliver instant access to funds, real-time notifications, and intuitive mobile experiences, while open banking uses standardized APIs to securely share financial data with third parties. Together, they enable personalized insights, consolidated account views, automated budgeting, and seamless payments—fostering greater choice and competition in fintech.

What impact do AI in finance and blockchain payments have on fintech disruption and payment settlement?

AI in finance powers smarter credit scoring, fraud detection, and personalized guidance, speeding approvals and reducing risk. Blockchain payments offer near-instant settlement and transparent cross-border transfers. Together, these technologies drive fintech disruption by enabling faster, safer, and more efficient financial services, though governance, privacy, and interoperability are important considerations.

| Section | Key Points | Benefits / Impact | Examples / Notes |

|---|---|---|---|

| Overview of FinTech technologies | Intersection of finance and technology enabling new ways to handle money, manage risk, and deliver services. Core elements include cloud platforms, robust APIs, machine learning, artificial intelligence, mobile interfaces, and trusted data practices. Enables rapid payments, innovative credit scoring, open banking, and blockchain-based settlements. | Increases efficiency, reduces friction, expands access, and accelerates innovation across financial services. | Cloud platforms, APIs, ML/AI, mobile experiences; trusted data governance; support for payments, credit scoring, open banking, and blockchain settlements. |

| Rise of digital banking innovations | Banks and fintechs shift from branches to app-led, user-centric experiences. Users expect instant access to funds, real‑time notifications, and seamless cross‑border transfers. Institutions deploy fast payments rails, intuitive interfaces, and biometric authentication. | Improved customer experience and engagement; lower operating costs; faster, more convenient services. | Digital-first banks, challenger brands, mobile apps, biometric login. |

| Open banking as ecosystem accelerator | Secure access to financial data via standardized APIs; banks, fintechs, and other providers build innovative products atop existing accounts. Fosters competition, collaboration, and new revenue streams. | More choice and better pricing for consumers; personalized tools; account aggregation and cash-flow insights. | Budgeting apps, automated savings, cash-flow optimization, account linking. |

| AI in finance | AI/ML enable richer credit scoring, adaptive fraud detection, and personalized advice via chatbots. Models forecast liquidity and optimize pricing; faster approvals; governance and bias concerns. | Faster decisions, reduced fraud, more relevant product recommendations; need for transparent governance to mitigate bias. | Chatbots, risk scoring with rich data, explainable AI initiatives. |

| Blockchain payments & settlement | Distributed ledger tech enables near-instant settlement, lower reconciliation costs, and greater transparency. Smart contracts automate compliance and terms; cross-border payments and settlement models evolve. | Faster, cheaper, more transparent value transfer; new business models and settlement capabilities. | Cross-border payments, smart contracts, trade finance, remittances. |

| RegTech & risk management | RegTech tools help monitor compliance, manage risk, and govern complex operations. Emphasis on data privacy, cybersecurity, and identity verification. | Improved compliance, reduced risk exposure, and enhanced trust; governance and privacy are central. | Data encryption, consent management, auditable processes. |

| Benefits for consumers and businesses | Faster payments, lower costs, real-time balance visibility; for businesses, efficiency gains, better cash flow, and new channels. SMEs gain from open APIs for invoicing, reconciliation, and credit access. | Enhanced financial health, inclusivity, and growth opportunities for both individuals and organizations. | Real-time updates, instant lending decisions, automated reconciliation. |

| Challenges & considerations | Security is paramount; interoperability with legacy systems; talent and culture; regulatory compliance; data residency and cross-border data flows. | Addresses risk and implementation hurdles; successful adoption depends on robust governance. | Strategic integration plans, governance frameworks, and data strategies. |

| Case studies in digital transformation | Banks and fintechs collaborate to deliver richer services: open banking-enabled dashboards, consolidated finances, automated savings; blockchain-based settlements; AI-powered underwriting. | Demonstrates tangible benefits: faster service, better pricing, improved risk management. | Digital banks with open APIs; payments via blockchain; AI underwriting in insurance. |

| What organizations should do to embrace FinTech technologies | 1) Customer-centric roadmap; 2) Modular API-driven architecture; 3) Data governance & security; 4) Responsible AI; 5) Pilot, measure, scale; 6) Regulators & industry collaboration. | Supports scalable, trusted implementation and ensures alignment with rules and customer needs. | Step-by-step guidance for roadmap and architecture. |

| Future outlook | Embedded finance, broader AI decisioning across insurance, investment, and wellness; continued open banking and data sharing; evolving blockchain-based settlement; interoperability and regulation. | Deeper integration, broader adoption, and focus on trustworthy, human-centered experiences. | Embedded finance, standard data sharing, and interoperable ecosystems. |

Summary

End of table.