Taxation Tips for Cryptocurrency Gains are essential in a market that evolves fast. As crypto markets evolve and more investors participate, understanding how the tax system treats digital assets is essential for accurate reporting. This guide helps you interpret taxable events and capital gains tax crypto implications, calculate gains, and stay compliant while reducing surprises at tax time. By focusing on practical steps, you can reduce surprises at tax time and keep your tax burden manageable. From cost basis to record-keeping, these tips cover the key aspects of crypto tax rules and reporting.

Beyond the basics, the topic can be framed in alternative terms such as digital asset taxation, virtual currency gains, and prudent record-keeping. This framing aligns with Latent Semantic Indexing by tying in IRS reporting for cryptocurrency and crypto tax deductions to the same underlying obligations. By focusing on practical steps like maintaining cost basis records, lot identification, and timely documentation, you can simplify compliance and risk management. In addition to holding strategies, long-term planning and careful reporting help minimize liabilities while staying within the rules.

Taxation Tips for Cryptocurrency Gains: Navigating Crypto Taxes, Cost Basis, and Reporting

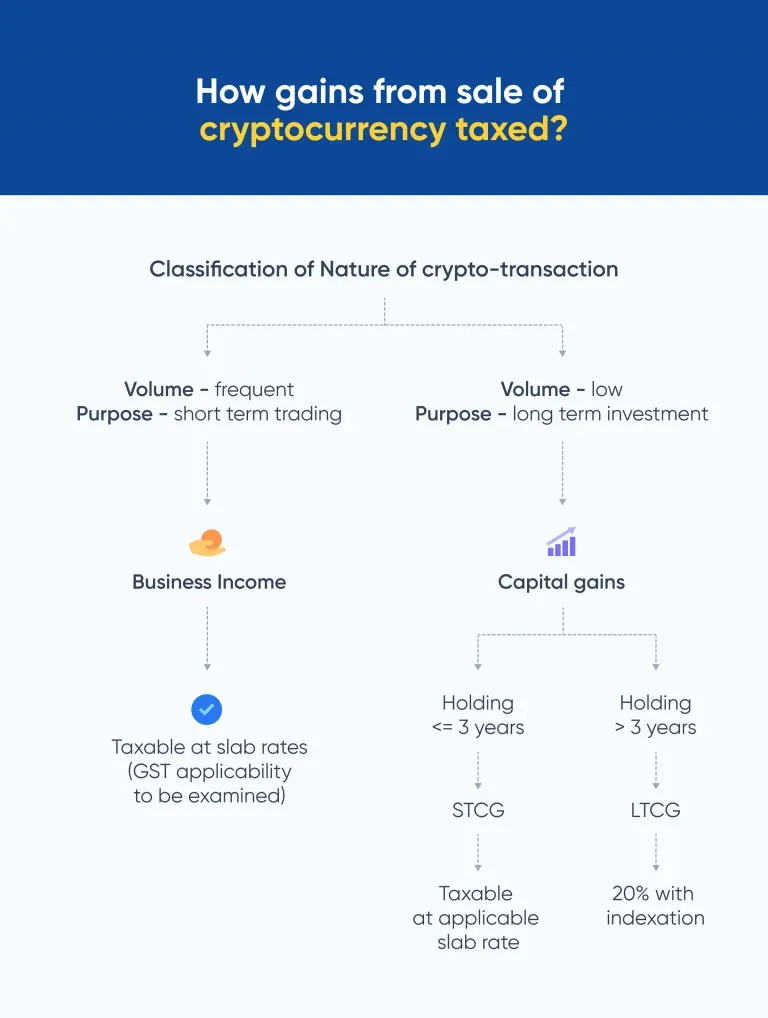

Taxation Tips for Cryptocurrency Gains helps investors understand how taxable events in crypto trigger either ordinary income or capital gains taxes, depending on activity and holding period. By recognizing events such as selling for fiat, exchanging one crypto for another, using crypto to purchase goods or services, mining and staking rewards, and even some hard forks or airdrops, you can anticipate tax obligations and plan accordingly. This framing also aligns with crypto taxes best practices, emphasizes clear cost bases, and keeps you aware of how capital gains tax crypto treatment varies with holding duration.

Keeping accurate records is the foundation of compliant crypto tax reporting. Track acquisition dates, cost basis, sale proceeds, and fees, and maintain on-chain evidence and exchange logs to support your calculations. When you understand your cost basis and the specific identification method you’ll use, you reduce surprises at tax time and improve IRS reporting for cryptocurrency activities. Distinguishing income events (like mining or rewards) from capital gains events is essential for correct tax treatment and smoother filing.

Understanding the practical distinction between short-term and long-term gains guides planning strategies as you build or rebalance a portfolio. Short-term gains are typically taxed at ordinary income rates, while long-term holdings may enjoy preferential rates in many jurisdictions. This awareness informs decisions about holding periods, tax planning, and how to structure transactions to optimize tax outcomes within the bounds of tax compliance for cryptocurrency.

Maximizing Crypto Tax Deductions and Compliance: Practical Steps for Tax Compliance for Cryptocurrency

Beyond reporting gains, you can pursue legitimate crypto tax deductions by tracking costs related to your activity, including exchange fees, wallet security expenses, and certain professional services. Charitable donations of appreciated crypto can also offer tax benefits, allowing you to donate without triggering capital gains taxes and still claim a deduction for fair market value. These deductions, alongside well-documented records, contribute to a more favorable tax outcome while staying compliant with current rules.

A strategic approach to tax planning includes tax-loss harvesting, long-term holding when feasible, and utilizing specific identification to select the most advantageous lots. Using reputable tax software or working with a tax professional who understands crypto helps ensure accurate IRS reporting for cryptocurrency and minimizes the risk of penalties. Distinguishing personal from business crypto activity, staying current with evolving crypto taxes regulations, and maintaining organized documentation all support tax compliance for cryptocurrency in practice.

Finally, maintain an annual review of your strategy to adapt to changing regulations, rates, and reporting requirements. Regular updates help you stay aligned with crypto taxes expectations, optimize deductions such as crypto tax deductions, and ensure you’re prepared for the IRS reporting for cryptocurrency obligations when tax season arrives.

Frequently Asked Questions

What are the essential crypto taxes and IRS reporting for cryptocurrency steps to follow under Taxation Tips for Cryptocurrency Gains?

Key steps include identifying taxable events (selling crypto for fiat, exchanging one crypto for another, using crypto to buy goods or services, and mining or staking rewards). Distinguish capital gains from ordinary income (short-term vs long-term). Maintain accurate cost basis and apply Specific Identification when possible. Keep detailed records of dates, amounts, fees, and values. Report capital activities on Form 8949 and Schedule D, and report ordinary income from mining or staking on the appropriate lines of Form 1040. Stay compliant by regularly updating records and consulting current guidance as rules evolve.

How can I improve tax compliance for cryptocurrency while leveraging crypto tax deductions and Taxation Tips for Cryptocurrency Gains?

Focus on practical strategies: use tax-loss harvesting to offset gains; consider long-term holding for favorable tax rates; apply Specific Identification to select the most advantageous lots. Take advantage of crypto tax deductions where eligible, including charitable donations and deductible expenses related to exchanges, wallets, or professional services. Maintain meticulous documentation and use crypto-aware tax software or a qualified professional. Separate personal and business crypto activity, and review your tax strategy annually to stay aligned with evolving crypto tax rules and IRS reporting for cryptocurrency.

| Topic | Key Points |

|---|---|

| Taxable events | Selling crypto for fiat, exchanging one crypto for another, using crypto to buy goods or services, mining or staking rewards, and hard forks/airdrops; these events can trigger ordinary income or capital gains depending on activity and holding period; maintain accurate records and classify each event as income or capital gain. |

| Cost basis and identification | Cost basis is what you paid (including fees) and affects gains/losses; Specific Identification lets you designate the exact lot sold if supported; if not, default methods or averages may apply by jurisdiction. |

| Staying organized | Staying organized means keeping dates, amounts, counterparties, fees, fair market values, and on-chain data; wallet addresses and exchange logs help reconstruct your tax position. |

| Calculating gains and losses | Calculating gains involves tracking cost basis per lot; short-term vs long-term depends on holding period; use Specific Identification to optimize; maintain a detailed gain/loss ledger; mining/staking income is ordinary income when received. |

| Reporting crypto activity | Reporting involves categorizing gains and income and filing with the appropriate forms; in the US, Form 8949 and Schedule D for capital gains, Form 1040 for ordinary income; separate personal vs business activity; keep thorough records to reduce penalties. |

| Tax planning strategies and deductions | Tax planning strategies include tax-loss harvesting, long-term holding to reduce rates, specific lot identification, charitable donations, deductible expenses, documentation/software, and professional guidance; stay up to date with evolving rules. |

| Common mistakes to avoid | Common mistakes include not reporting activity; miscalculating basis; treating a sale as a new asset purchase; underreporting mining/staking income; ignoring cross-border tax implications. |

| Practical steps to stay compliant | Practical steps include real-time records, separating personal and business activity, using crypto-friendly tax software, consulting a tax professional, and reviewing strategy annually. |

Summary

Taxation Tips for Cryptocurrency Gains emphasize proactive planning and precise reporting as the foundation for compliant crypto taxation. By understanding what counts as a taxable event, keeping accurate cost bases, and applying sensible planning strategies, you can navigate reporting requirements with greater confidence. The guide underscores the importance of meticulous records, correct lot identification, and timely engagement with tax software or professionals to stay aligned with evolving rules. With disciplined practice—tracking transactions, separating personal and business activity, and reviewing strategies annually—you can optimize your tax outcomes while remaining compliant and focused on your crypto journey.